An Optimal Tax Plan for a Suboptimal Federal Budget

Growth-inducing provisions deserve permanent extensions. Other provisions should have shorter, temporary extensions

The last time Republicans held unified control of the government, they passed the Tax Cuts and Jobs Act of 2017 (TCJA). At the time, federal deficits stood at 3.4 percent of GDP. With deficits now at 5.2 percent, the stakes are higher as Congress considers extending TCJA provisions.

Failing to extend the TCJA is tantamount to a tax hike. Though some deductions would return, most households would see higher taxes due to higher tax rates and the loss of certain credits. While corporations would retain the 21 percent tax rate, the immediate expensing of investment would be gone, while TCJA’s permanent denial of expensing to R&D would remain. Pass-through businesses, which are not organized as corporations but have direct impacts on household tax returns, will also see tax increases.

An outright extension, however, would carry significant fiscal consequences. The Congressional Budget Office (CBO) and the Joint Committee on Taxation (JCT) estimate that a wholesale ten-year extension would add $4 trillion to federal deficits before factoring in rising interest payments. Although they likely underestimate offsets due to the impacts of tax rates on taxable income, investment, and growth, there’s no question that renewing the TCJA without spending cuts would increase deficits.

Lawmakers should avoid an all-or-nothing approach and instead follow a clear principle: provisions focused on economic growth deserve long-term extensions while provisions that aren’t as growth-inducing should have shorter extensions. Instead of the proposal currently on the table to extend the entire TCJA temporarily, they should pick and choose.

This strategy echoes the concept of the TCJA’s original design, which permanently reduced corporate tax rates and shifted the treatment of multinational corporations more to a territorial regime. Recent work by Jonathan Hartley, Joshua Rauh, and Kevin Hassett confirms the soundness of this approach. Their analysis found that corporate rate reductions significantly increased corporate investment, surpassing CBO's assumptions. Presumably the architects of the TCJA would have preferred to make even more provisions permanent, but when forced to choose, they chose the ones that they expected to be most pro-growth to make permanent.

A similar philosophy is needed in 2025.

Lawmakers may be wary about having to revisit the tax debate again and take a stance on which provisions are actually pro-growth. It’s easier for them just to punt and extend the entire package temporarily. But today’s fiscal problems are a consequence of modern Congresses avoiding their responsibility to be active participants in the budget process. Instead, with two-thirds of federal spending and much of the tax code set on autopilot, long-retired politicians largely control the nation’s budget.

Temporary extensions in general force lawmakers to confront spending. President Trump has promised significant spending cuts. If he succeeds, Congress could cement permanent tax cuts on a broader set of measures. Without significant spending restraint, however, tax cuts that are labeled permanent will prove not to be, as future taxpayers will have to bear the burden of deferred obligations either through higher explicit taxes or monetization of obligations through inflation.

Budget effects of the main TCJA measures of course fall dramatically with shorter extensions. Using CBO and JCT projections, a one-year extension of all TCJA provisions would add $470 billion to non-interest deficits. A five-year extension—pushing sunsets to 2030—would come in below $3 trillion over ten years.1

A tailored approach would be even better. Table 1 shows the deficit effects for one-, five-, and ten-year extensions of specific provisions.

Some provisions, like bonus depreciation deserve a permanent extension given their economic benefits and manageable fiscal impacts. The ten-year deficit effect of extending bonus depreciation is also relatively small: $378 billion. As Figure 1 shows, the budget effects are front loaded, as bonus depreciation simply shifts forward the timing of when businesses claim deductions for capital purchases. That makes a permanent extension a viable option even under reconciliation rules. Congress should also act to fully restore R&D expensing, as TCJA’s limits to the deductibility of R&D expenses are already dampening R&D.

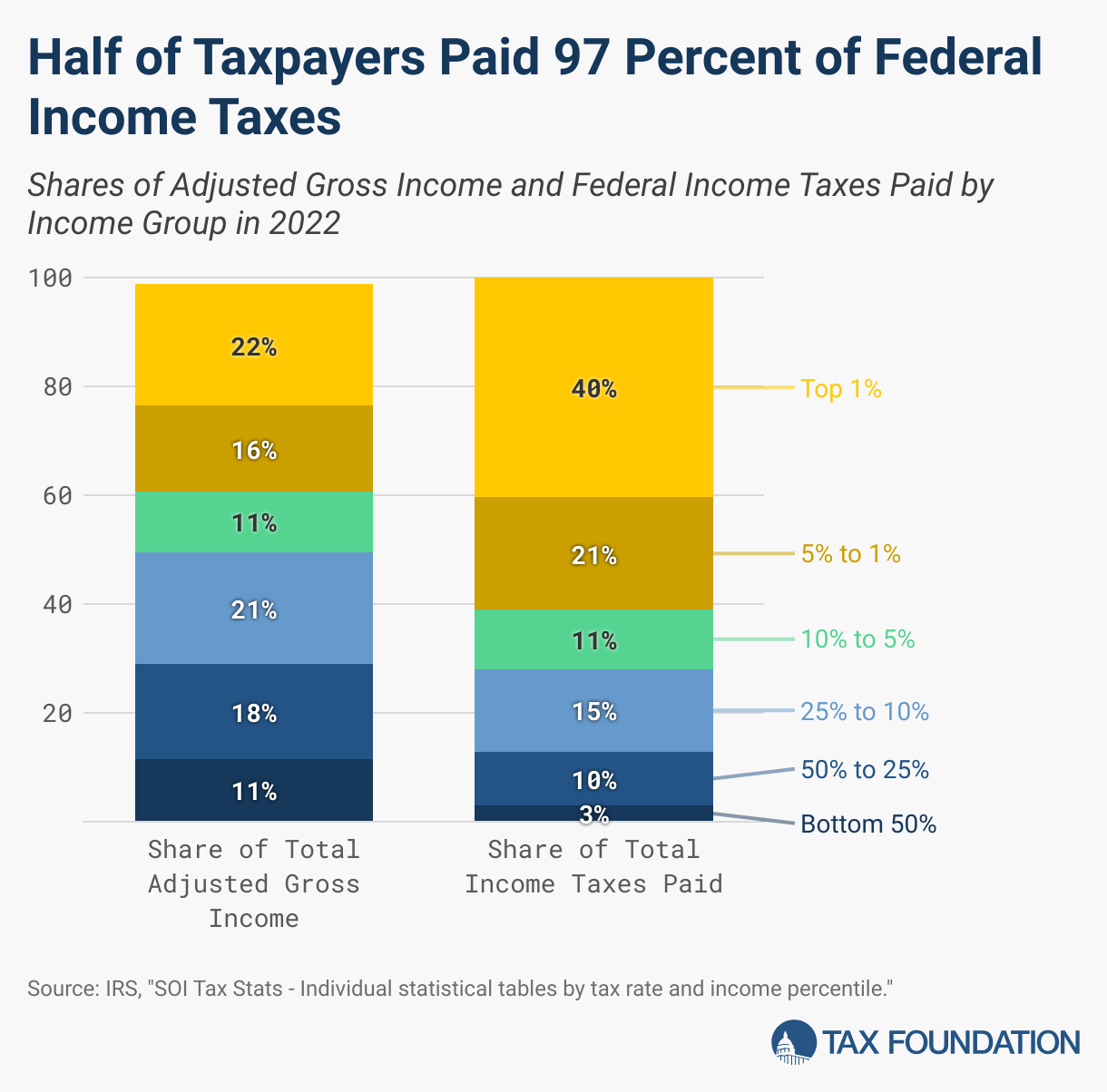

The household rate reductions are likewise important for growth, albeit with a higher official price tag. CBO and JCT expect extending the lower rates and brackets would add $2.2 trillion to non-interest deficits over ten years. The congressional scorekeepers, however, assume that taxpayers are relatively insensitive to changes in their tax rates. This is at odds with recent research by Josh Rauh and Ryan Shyu on California tax increases, which finds high-income filers are much more sensitive to rate changes than CBO and JCT assume. Considering that the top 1 percent of taxpayers pay 40 percent of federal income taxes, these estimates suggest that lower rates could be maintained with deficit effects much smaller than predicted.

{kind=link}

A permanent extension of the most pro-growth elements of the plan would be challenging under reconciliation rules, which prohibit increasing federal deficits beyond the ten-year budget window. In 2034, the final year of the CBO’s projections, rate reductions and bonus depreciation are projected to reduce revenue by $305 billion.

But the budget math can work if Congress makes TCJA’s base-broadening measures permanent. These provisions—including the cap on state and local tax (SALT) deductions, limits on mortgage interest deductions, and the repeal of the personal exemption—are projected to generate $400 billion in revenue in the final year of the budget window.2 That’s nearly $100 billion more than the expected revenue loss from the most pro-growth provisions. This leaves room for Congress to reform the SALT cap, making it permanent while potentially raising the cap to address concerns from high-tax states.

In contrast, provisions like the child tax credit, the expanded standard deduction, lower exemptions for the alternative minimum tax (AMT), and qualified business income deduction offer limited economic growth but carry substantial fiscal implications. Combined, CBO expects these provisions would add $4 trillion to federal deficits over ten years. These provisions are unambiguously tax cuts, and in the case of the expanded standard deduction and AMT, they represent worthwhile efforts to simplify the nation’s tax code. But, as the Tax Foundation has noted, their effects on growth are small relative to their budget effects. A shorter extension would balance Republicans’ objectives to extend the tax cuts with the need to address fiscal realities.

The same logic applies to President Trump’s campaign promise to eliminate taxes on tips, overtime, and Social Security benefits. According to the Committee for a Responsible Federal Budget, these tax breaks could reduce revenue by as much as $5 trillion over ten years. Though the merits of these tax breaks are debatable, if the Trump Administration insists, limiting them to one or two years would better suit the fiscal climate.

At its core, effective budgeting hinges on setting clear priorities. Congress hasn’t done that for many years. While lawmakers may benefit politically from avoiding contentious decisions, future taxpayers cannot afford continued inaction. Permanent extensions of some provisions combined with temporary extensions of others represent a balanced approach, combining economic growth, fiscal responsibility, and the necessity for ongoing oversight.

The estimates are derived from CBO (2024), Budgetary Outcomes Under Alternative Assumptions About Spending and Revenues. https://www.cbo.gov/publication/60114. The CBO score provides annual fiscal year (FY) deficit effects, which creates challenges when analyzing an earlier sunset due to lagged effects (e.g., a 2028 tax year sunset affects tax payments in FY2029). To address this issue, we incorporate the Joint Committee on Taxation’s (JCT) 2017 estimates for the major sunsetting provisions of the TCJA for 2025 and 2026. The percentage change between those two years is applied to approximate the impact in the year immediately following a sunset.

The actual revenue change will depend on which other provisions are extended. Returning the standard deduction to pre-TCJA levels would increase the revenue estimate from the limits on itemized deductions, while restoring pre-TCJA Alternative Minimum Tax exemption amounts would reduce it.

| A guest post by

|