Pensions vs Classrooms in Massachusetts: Part 2

How a switch to 401(k)-type plans could be accomplished with an employer contribution rate of 10%, and why the public must demand it

This week in the Boston Globe, we published an opinion piece entitled “Pensions vs. classrooms: Rising retirement costs are squeezing Massachusetts education.” The article is based on findings from our recent Hoover Institution report on how pension contributions are affecting education financing in six populous states around the country.

The bottom line of the report is that from 2015-2022, pension contributions as a percentage of associated education expenditures have increased significantly, by two percentage points of those total budgets across the states we studied. In Massachusetts, however, the increase was much larger, from 9.2% to 14.1%, or almost five percentage points of all related education expenditures.

In our opinion piece, we recommend that Massachusetts stem the rising tide of red ink by moving new school employees from traditional defined benefit pension plans to 401(k)-style plans. We may sound like a broken record, but it is time for legislators and citizens to prioritize this and demand it before things get much worse. Here we discuss specifically how such a change could be accomplished.

In Massachusetts, the state picks up the tab for the employer share of teachers’ pension contributions, unlike in most other states where the school districts also must contribute. The increasing demands of pensions are therefore a direct drain on cash that could be used more directly for education. When school districts do not share directly in the costs, they have less incentive to pay attention to those costs, since they have no control over exactly how the state would spend or distribute the savings. This dynamic likely has contributed to the faster pace of escalation of pension costs in Massachusetts compared to other states.

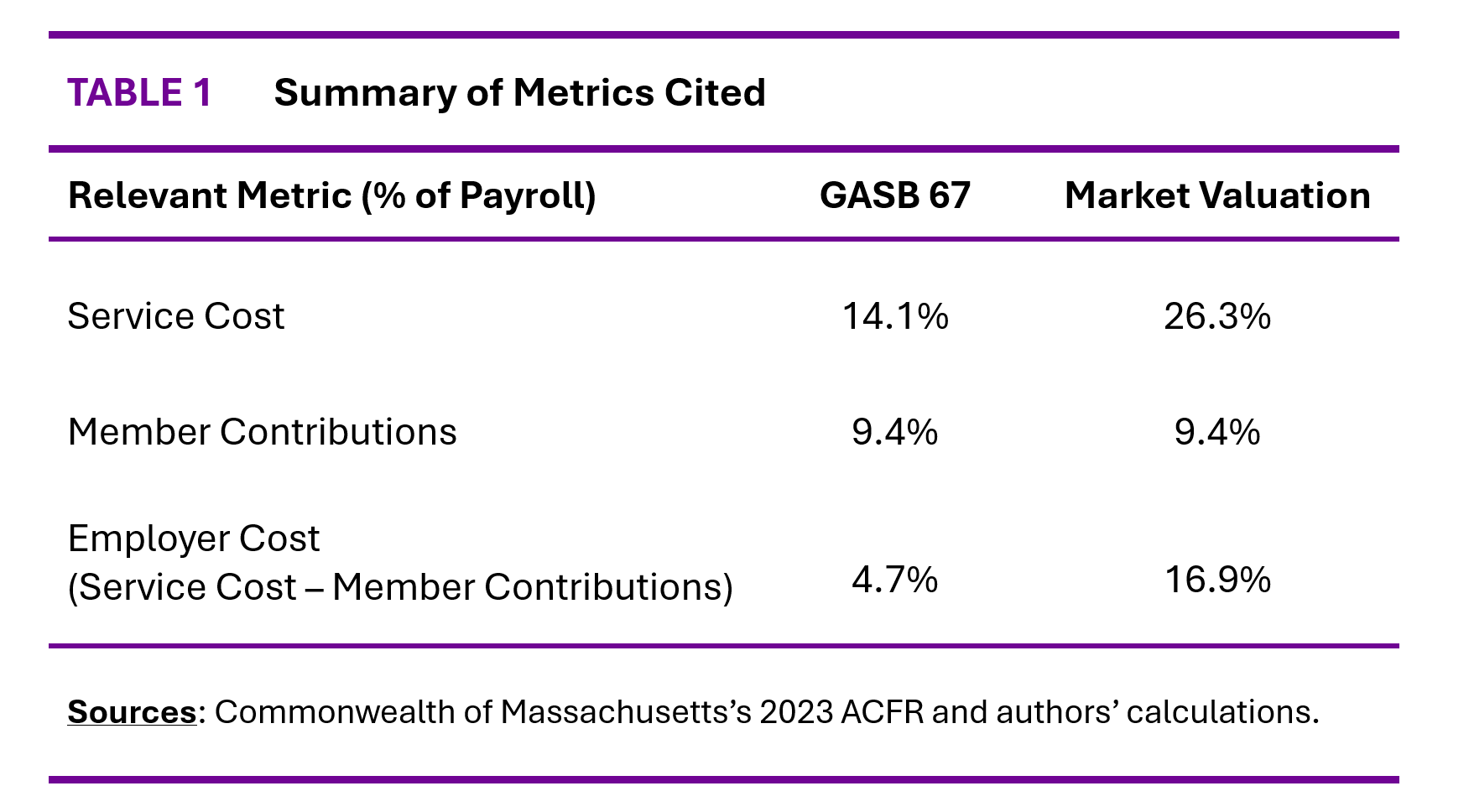

How much is the Massachusetts Teachers Retirement System (MTRS) pension plan actually costing the state per employee as a percent of pay? In 2023, the state contributed $2.15 billion. While our report focuses on scaling by total related education expenditures, another way to present this figure is that it is 25.7% of the payroll of teachers and other school staff, based on figures in the state’s GASB 67 reports. Most teachers contribute 11% of pay, but according to the state’s latest GASB 67 report the employee contributions amounted to 9.4% of payroll.

Adding the state and employee contributions together, total pension contributions amount to 35.1% of pay.

If this is the cost of the plan, a natural question is what else could be done with 35.1% of employee pay instead. However, this is not quite the right comparison for thinking about a replacement plan. Some portion of the 35.1% is related not to compensation for current work but rather to catching up on past (“legacy”) promises, which the state would have to do anyway even if it introduces new plans.

Based on the state’s disclosures, the so-called “service cost”, or cost of running the MTRS without considering these catch-up contributions, amounts to 14.1% of pay. Subtracting the teachers’ own contributions, the employer cost would only amount to 4.7% of payroll.

This figure – a roughly 4.7% of pay “employer cost” of the DB plan – tends to anchor discussions around reforms and possible replacement plans. Taking it at face value, one might mistakenly think that any plan where the employer must contribute more than 4.7% of payroll would not save money for the state.

The problem is that such calculations understate the true cost of continuing to offer the plan because the state makes aggressive assumptions about investment returns, namely an investment return of 7% per annum. Applying the principles of financial valuation, which use default-free government bond yields to discount default-free promises, we find that the true service cost is 26.3% of payroll, not 14.1% of payroll. Subtracting off the 9.4% teachers’ own contributions, the employer service cost amounts to 16.9% of payroll, not 4.7% of payroll.

The point of all this is that based on flawed estimates of costs, one might believe that a 401(k)-type plan with employer costs of more than around 5% of payroll wouldn’t save money. In fact, even if the state had to contribute almost 17% of pay to the 401(k)-type plan, there would still be considerable cost savings. Furthermore, in the 401(k)-type plan the state cannot kick the costs down the road so that they balloon with every year that passes, which is why the state is at the point it is now with total contributions hitting 35% of pay.

Fortunately, there are sensible 401(k)-like retirement plan structures that would cost the state less than 16.9% of pay, and teachers less than 9.4% of pay.

At present, teachers are not covered by Social Security. Without pension checks, including them in the system would make sense. This would cost 6.2% each for employer and employee. If in addition there were a 401(k)-type plan where the state made a 10% contribution and employees made a 3% contribution, both the state and teachers would be contributing less.

For most employees, receiving an employer contribution of 10% of their pay each year in a tax-deferred retirement account that they can bring with them even if they switch jobs (unlike the current pension arrangement) is an appealing prospect.

Concerned Massachusetts taxpayers are looking at an uphill battle in affecting change to the present system. Massachusetts courts have historically upheld strong protections for public employees’ pensions, and to the extent changes have been allowed they have largely impacted new employees. In 1973 the Massachusetts House of Representatives requested an advisory opinion from the Massachusetts Supreme Court when representatives were considering raising the employee contribution rate from 5% to 7%. The court advised that material increases to contributions without commensurate increases to benefits would be considered “presumptively invalid.” Legislative changes from this point have thus been able to raise contribution rates, but only for prospective employees.

Furthermore, since proposals that concern the appropriation of funds are excluded from ballot measures, changes of this sort would likely need to originate within the state legislature not with a citizen’s ballot initiative. To the extent the legislature did pursue a change, the effort would face legal challenges from the state’s teachers’ union. Even if it only affects new employees, the pension has often been viewed as an aspect of solidarity by the union, and keeping new employees in the plan also allows the cash they put in to be used to pay benefits for current generations of retirees, similar to a pyramid scheme. But of course, the people who are hurt the most by the opposition to pension reform and are most vulnerable to a serious fiscal crisis in the state are those with the largest part of their careers ahead of them.

Absent significant public engagement against the growing burden of pension liabilities on the state’s budget, education resources will be increasingly consumed by pension contributions, pushing the state closer to fiscal calamity.

| A guest post by

|